I’m Self-Employed in Idaho Falls. What Health Insurance Options Do I Actually Have?

If you’re self-employed in Idaho Falls, health insurance can feel confusing fast.

Maybe you run a small business. Maybe you’re a contractor, consultant, freelancer, real estate professional, hairstylist, truck driver, farmer, gig worker, or solo operator. Maybe you recently left a job and no longer have employer coverage.

Whatever your situation, the question is usually the same:

“What health insurance options do I actually have?”

The good news is that self-employed people do have real options. The harder part is knowing which option fits your income, household, doctors, prescriptions, and budget.

For people comparing health insurance Idaho Falls options, the main choices usually include ACA Marketplace plans through Your Health Idaho, off-marketplace individual health plans, coverage through a spouse or household member’s employer plan, Medicaid or Medicare if eligible, and sometimes small-group coverage if the business has eligible employees.

Your Health Idaho is Idaho’s official health insurance marketplace. It allows individuals and families to shop, compare, and enroll in health insurance plans, and it is the only place Idahoans can receive a tax credit to lower monthly premiums.

This guide explains the main options in plain English so you can make a more confident decision before choosing a plan.

Why Health Insurance Feels Different When You’re Self-Employed

When you work for an employer, health insurance often shows up as part of your benefits package. You may still have choices, but the employer usually narrows the plan list and may pay part of the premium.

When you’re self-employed, you often have to make the decision yourself.

That means you may need to compare:

- Monthly premiums

- Deductibles

- Copays

- Coinsurance

- Prescription coverage

- Doctor and hospital networks

- Household income estimates

- Tax credit eligibility

- Coverage for family members

- Out-of-pocket exposure if something serious happens

This is where many self-employed people get stuck. A plan with the lowest monthly premium may not be the best fit if the deductible is too high, your doctor is out of network, or your prescriptions are not covered well.

ACA Marketplace coverage plays an important role for people who do not have employer-sponsored insurance. CMS reported that 24.3 million consumers selected or were automatically re-enrolled in Marketplace coverage during the 2025 Open Enrollment Period, a 13% increase from 2024.

That matters because many self-employed people rely on individual health coverage rather than traditional employer benefits. KFF has also reported that many ACA Marketplace enrollees are connected to small businesses or self-employment, including small business owners, employees, and self-employed workers.

For Idaho Falls workers without employer coverage, comparing individual health plans is not just a paperwork task. It is a real household and business decision.

Your Main Health Insurance Options If You’re Self-Employed in Idaho Falls

The right option depends on your income, household size, eligibility, doctors, prescriptions, and whether you need coverage for yourself or your family.

Here is a simple breakdown.

The most common starting point for many self-employed people is the individual health insurance market.

HealthCare.gov explains that the Individual Marketplace offers coverage for people who run their own businesses, are self-employed with no employees, or work as freelancers or consultants.

In Idaho, that Marketplace is Your Health Idaho.

Option 1: ACA Health Plans Through Your Health Idaho

For many self-employed people in Idaho Falls, ACA health plans are the first option to review.

ACA plans are often called Marketplace plans. In Idaho, people shop for these through Your Health Idaho, not the federal HealthCare.gov enrollment platform.

Your Health Idaho states that every plan offered through the marketplace is required to cover ten essential health benefits, including doctor visits, hospitalization, and preventive wellness.

This matters because self-employed people often worry about whether an individual plan is “real insurance.” ACA-compliant Marketplace plans must follow federal rules for essential health benefits.

Why ACA Health Plan Assistance Can Matter

The biggest reason to look at Your Health Idaho is tax credit eligibility.

The Idaho Department of Insurance says premium subsidies, also called advanced premium tax credits, are available only when the health benefit plan is purchased through Your Health Idaho.

That does not mean everyone qualifies for a tax credit. It means that if you do qualify, Your Health Idaho is where Idahoans access that help.

For self-employed people, income can change from month to month. That makes the application process more important because Marketplace savings are based on estimated income for the year of coverage.

HealthCare.gov explains that self-employed people must estimate net self-employment income, and Marketplace savings are based on estimated net income for the year they are getting coverage, not last year’s income.

That is one of the most common places people need help. If you estimate too high, too low, or forget to update income changes, it can affect your tax credit and what happens when you file your taxes.

Option 2: Off-Marketplace Individual Health Plans

Some self-employed people also compare individual health plans outside Your Health Idaho.

The Idaho Department of Insurance says insurance companies may offer individual health benefit plans through Your Health Idaho, off the marketplace, or both. It also states that premium subsidies are available only when the plan is purchased through Your Health Idaho.

So, the basic difference is this:

An off-marketplace plan is not automatically better or worse. It simply needs to be compared carefully.

For example, someone may prefer a certain carrier, network, or plan structure. Another person may benefit more from checking tax credit eligibility through Your Health Idaho. The right answer depends on the person.

This is where working with a local insurance agency near Idaho Falls can help. A local advisor can help you compare available options without making the decision only about the premium.

Option 3: Coverage Through a Spouse or Household Member’s Employer Plan

Some self-employed people can join a spouse’s employer health plan.

That can be a good option in some cases, but it still needs a careful review. Employer plans may have different rules for employee-only coverage and family coverage. Sometimes the employee’s cost is reasonable, but adding a spouse or children can be much more expensive.

Before choosing this route, compare:

- The total monthly cost for the whole household

- Whether your doctors are in network

- Prescription coverage

- Deductibles and out-of-pocket limits

- Whether the plan works well for children or dependents

- Whether you are eligible for other options

Do not assume the employer plan is automatically the best choice. Also, do not assume an individual plan is automatically cheaper. You have to compare the real numbers.

Option 4: Medicaid, Medicare, or Other Coverage Based on Eligibility

Some self-employed Idaho residents may qualify for Medicaid, Medicare, VA coverage, or another type of health coverage depending on age, income, disability status, household situation, or other eligibility rules.

This article does not determine eligibility. That requires a personalized review.

For people approaching age 65, Medicare planning becomes especially important. For younger self-employed people with changing income, Medicaid eligibility may need to be reviewed based on current rules and household details.

The key point is simple: do not assume you are limited to one option until you review eligibility.

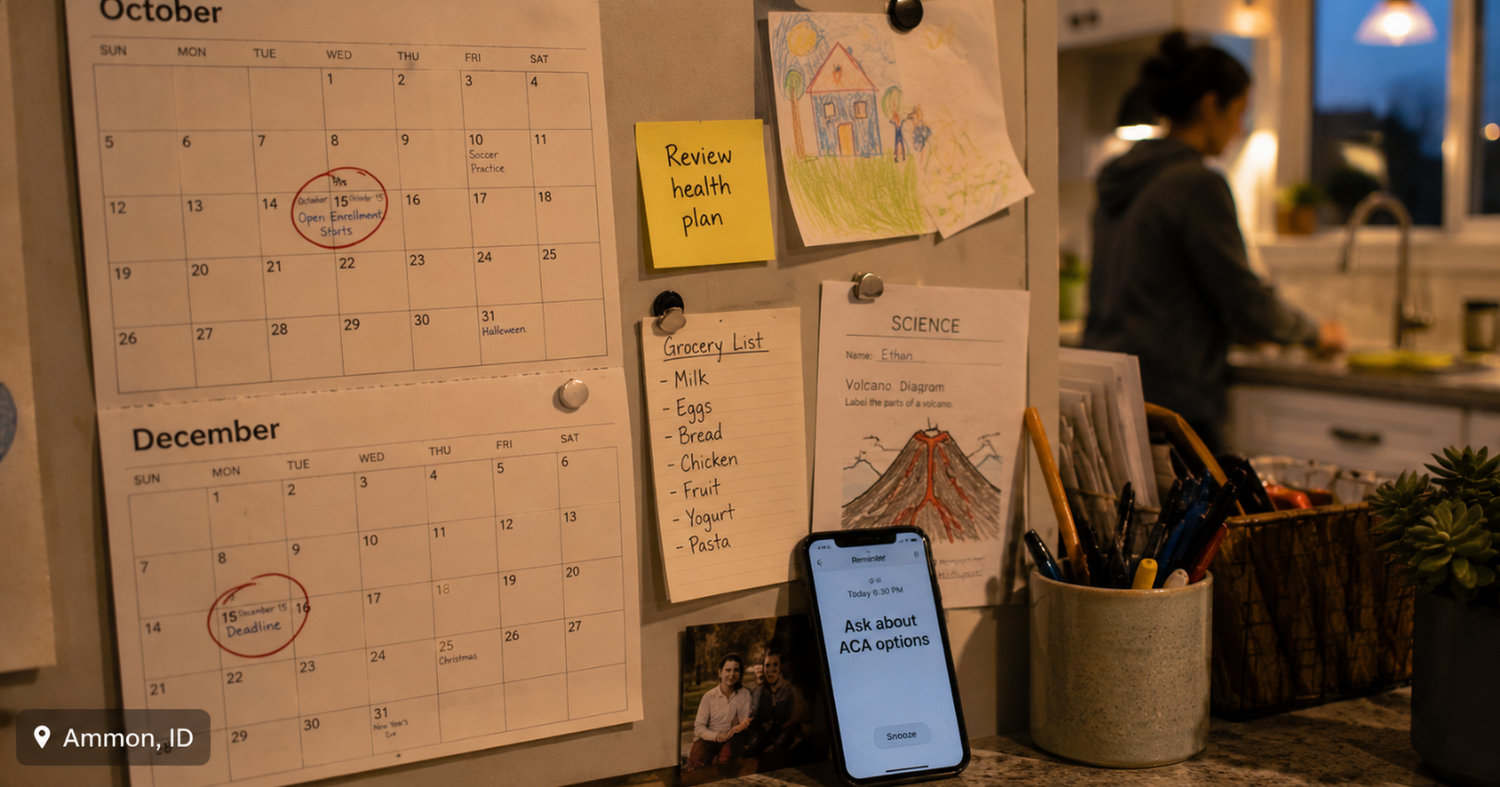

Open Enrollment and Special Enrollment in Idaho

Timing matters.

Your Health Idaho states that Open Enrollment takes place yearly from October 15 to December 15. During that period, Idahoans can apply for a tax credit and enroll in a health insurance plan for the coming year.

If you miss Open Enrollment, you may still be able to enroll if you qualify for a Special Enrollment Period.

Your Health Idaho explains that a qualifying life event, such as losing coverage, moving, getting married, or having a baby, may make someone eligible for a Special Enrollment Period outside Open Enrollment.

For self-employed people, common life changes may include:

- Leaving a job and losing employer coverage

- Moving to Idaho Falls, Ammon, Iona, or Ucon

- Getting married

- Having or adopting a child

- Losing other qualifying health coverage

- Changes in household situation

If one of these applies, it is worth asking about enrollment options instead of waiting until the next Open Enrollment period.

What Self-Employed People Should Compare Before Choosing a Health Plan

A lot of people search for health insurance near me because they want someone local to help them sort through the details.

That makes sense. Choosing a plan is not just about finding the cheapest monthly premium.

1. Monthly Premium

The premium is what you pay each month to keep coverage active.

A lower premium may look attractive, but it can come with higher deductibles, higher out-of-pocket costs, or a narrower network.

2. Deductible

The deductible is what you may need to pay before the plan starts paying for many covered services.

For self-employed people, this matters because a high deductible can affect cash flow if you have a medical event.

3. Out-of-Pocket Maximum

The out-of-pocket maximum is the most you pay for covered in-network services during a plan year, not counting premiums.

This number helps you understand your financial exposure in a bad medical year.

4. Doctor and Hospital Network

If you have doctors, clinics, specialists, or hospitals you prefer in Idaho Falls or Eastern Idaho, check the network before enrolling.

A plan is less helpful if your preferred providers are not included.

5. Prescription Coverage

If you take prescriptions, review the plan’s drug list and pharmacy rules.

Different plans may treat the same medication differently.

6. Tax Credit Eligibility

If you shop through Your Health Idaho, you may be able to check whether you qualify for a premium tax credit.

Your Health Idaho provides a tax credit estimator that asks for basic information such as zip code, birthdays for household members to be enrolled, and annual household income.

7. Cost-Sharing Reductions

Cost-sharing reductions may lower deductibles, coinsurance, and copayments for eligible people who choose a Silver plan.

Your Health Idaho explains that to qualify for cost-sharing reductions, income must be within a certain range of the Federal Poverty Level and the person must be enrolled in a Silver Tier Plan.

HealthCare.gov also explains that cost-sharing reductions lower deductibles, copayments, and coinsurance, and that eligible people must choose a Silver plan to receive those extra savings.

That is important because some people choose a Bronze plan for the lower premium without realizing they may be giving up possible cost-sharing help available only through Silver plans.

Common Mistakes Self-Employed People Make With Health Insurance

Mistake 1: Choosing Only by the Monthly Premium

A low premium can be helpful, but it is only one part of the cost.

A plan with a lower premium may have higher costs when you actually use care. For some people, that tradeoff is fine. For others, it creates stress later.

Mistake 2: Guessing Income Without a Plan

Self-employed income can be uneven.

HealthCare.gov says Marketplace savings are based on estimated net income for the year you are getting coverage.

That means your estimate should be thoughtful. If your income changes during the year, you may need to update your information.

Mistake 3: Forgetting to Check Doctors and Prescriptions

A plan may look good on paper but be frustrating if your doctor, clinic, specialist, pharmacy, or medication does not fit well with the plan.

Mistake 4: Missing Idaho’s Open Enrollment Window

Idaho’s Open Enrollment period runs from October 15 to December 15 through Your Health Idaho.

That is earlier than many people expect, especially if they see national information that does not apply exactly to Idaho.

Mistake 5: Assuming You Do Not Qualify for Help

Some people assume they will not qualify for a tax credit, so they never check.

Your Health Idaho is the only place Idahoans can receive a tax credit to lower monthly premiums.

The safest move is to review your actual situation instead of guessing.

A Simple Decision Framework for Idaho Falls Self-Employed Workers

Use this framework before choosing a plan.

Step 1: Define Who Needs Coverage

Are you covering only yourself? A spouse? Children? A whole family?

Household size affects plan choice and potential eligibility.

Step 2: Estimate Your Income Carefully

For self-employed people, use projected net self-employment income for the coverage year.

Marketplace savings are based on expected income for the year you want coverage.

Step 3: List Your Doctors and Prescriptions

Before comparing premiums, write down:

- Doctors

- Clinics

- Specialists

- Hospitals

- Prescriptions

- Preferred pharmacies

Step 4: Compare Total Risk, Not Just Monthly Cost

Look at the premium, deductible, copays, coinsurance, and out-of-pocket maximum.

This gives you a clearer picture of what the plan may cost if you actually need care.

Step 5: Ask Whether a Silver Plan Changes the Math

If you may qualify for cost-sharing reductions, review Silver plans carefully. Those reductions are tied to Silver plan enrollment.

Step 6: Get Local Help Before You Enroll

If you are unsure, talk with a local advisor before choosing. Health insurance choices can affect your household budget for the full plan year.

Why Local Help Matters in Idaho Falls and Ammon

Self-employed people in Idaho Falls, Ammon, Iona, Ucon, and nearby Eastern Idaho communities often have practical questions that a national call center may not answer clearly.

They may ask:

- Which plans include my local doctors?

- What if my income changes this year?

- Can I cover my spouse and kids?

- Should I use Your Health Idaho or look off marketplace?

- What happens if I miss Open Enrollment?

- Can I get help with ACA health plan assistance?

- How do I avoid picking a plan that looks cheap but costs more later?

Eagle Cap Insurance – Idaho Falls is located at 919 S 25th E, Suite 130, Ammon, ID 83406 and helps local individuals, families, and business owners compare coverage options.

For a self-employed person, that local guidance can save time and reduce confusion. The goal is not to push one plan. The goal is to understand your options and choose with confidence.

When Should You Review Your Health Insurance?

You should review your health insurance when:

- You become self-employed

- You leave a job with employer coverage

- You move to Idaho Falls, Ammon, Iona, Ucon, or Eastern Idaho

- Your income changes

- You get married or divorced

- You have or adopt a child

- Your prescriptions change

- Your doctor stops accepting your plan

- Your premium, deductible, or out-of-pocket costs increase

- Open Enrollment is approaching

- You feel unsure whether your current plan still fits

Health insurance is not something to set and forget. For self-employed people, an annual review is especially important because income, family needs, and plan options can change.

Frequently Asked Questions

What health insurance options do self-employed people have in Idaho Falls?

Self-employed people in Idaho Falls may be able to choose from ACA Marketplace plans through Your Health Idaho, off-marketplace individual health plans, coverage through a spouse’s employer plan, Medicaid or Medicare if eligible, or small-group options if they have eligible employees.

Where do Idaho residents shop for ACA health insurance plans?

Idaho residents shop for ACA Marketplace plans through Your Health Idaho, Idaho’s official health insurance marketplace. Your Health Idaho is also the only place Idahoans can receive tax credits to lower monthly premiums.

Can self-employed people qualify for health insurance tax credits?

Yes, some self-employed people may qualify for premium tax credits depending on household income and eligibility. HealthCare.gov explains that self-employed applicants estimate net self-employment income, and Marketplace savings are based on estimated income for the coverage year.

When is Open Enrollment for health insurance in Idaho?

Your Health Idaho states that Open Enrollment runs yearly from October 15 to December 15. During that period, Idahoans can apply for a tax credit and enroll in a health insurance plan for the coming year.

What if I miss Open Enrollment in Idaho?

You may still be able to enroll if you qualify for a Special Enrollment Period. Your Health Idaho says qualifying life events can include losing coverage, moving, getting married, or having a baby.

Should I choose the cheapest health insurance plan?

Not always. A lower premium may come with a higher deductible, higher out-of-pocket costs, or a provider network that does not fit your needs. Compare the full cost and coverage details before choosing.

What are cost-sharing reductions?

Cost-sharing reductions are discounts that can lower deductibles, copayments, and coinsurance for eligible people. Your Health Idaho and HealthCare.gov both explain that eligible consumers must choose a Silver plan to receive those savings.

Can Eagle Cap Insurance help with ACA health plan assistance in Idaho Falls?

Yes. Eagle Cap Insurance – Idaho Falls helps individuals, families, self-employed workers, and small business owners compare health insurance options and understand ACA health plan assistance.

Final Takeaway

If you’re self-employed in Idaho Falls, you are not stuck figuring out health insurance alone.

Your options may include ACA Marketplace coverage through Your Health Idaho, off-marketplace individual health plans, coverage through a spouse’s employer plan, Medicaid or Medicare if eligible, or group options if your business has employees.

The best choice depends on your income, household, doctors, prescriptions, budget, and eligibility. Before you choose, compare more than the monthly premium.

Eagle Cap Insurance – Idaho Falls can help self-employed individuals, families, and small business owners review health insurance plans, understand ACA health plan assistance, and compare options in plain English.

Schedule an appointment with Eagle Cap Insurance – Idaho Falls

Call: +1 208 529 1522

Visit the Idaho Falls / Ammon location page:

Disclaimer: This article is for general educational purposes only and does not replace personalized insurance advice. Coverage options, eligibility, plan availability, provider networks, and costs can vary.