Life Insurance in Idaho Falls: What Happens When You Wait Too Long?

The Cost of Waiting, Financially and Emotionally.

It happens more often than you’d think.

Someone in their late 40s, in good health, walks into our office in Idaho Falls ready to “finally” get a life insurance policy in place. A week later, they get flagged in underwriting for a heart arrhythmia they didn’t know about. Their application moves from “preferred” to “table-rated.” The cost triples.

Life insurance is one of those things you don’t realize you needed until it’s too late to get it on your terms.

At Eagle Cap Insurance, we’ve guided Idaho families through every version of this story, whether you’re raising kids, building a business, or thinking about your legacy.

If you’re in Preston, Idaho Falls, or somewhere nearby, here’s what you need to know.

Why Idaho Families Put This Off? (And Why It’s Risky?)

Most people don’t avoid life insurance out of neglect. They’re just not sure where to start, or assume it’s expensive, complicated, or only necessary “later.”

But here’s what we see on the ground in Idaho Falls and Preston:

- A young family loses a breadwinner unexpectedly. No policy in place.

- A single dad puts off coverage and is diagnosed with diabetes, rates double.

- A business partner passes without a buy-sell funded, leaving the co-owner in a financial scramble.

Life insurance isn’t for you, it’s for the people you care about.

The Financial Ripple Effect of No Coverage

Let’s look at a basic scenario:

- Idaho Falls family of four

- $5,000 monthly household expenses

- $300,000 remaining mortgage

- Kids aged 9 and 12

If the primary income earner passes away with no coverage:

- Social Security survivor benefits may only cover ~$2,000/month

- The rest? It’s on the family, unless they’ve got life insurance.

We’ve seen families launch GoFundMe pages overnight. We’ve also seen parents get 20-year term policies for under $50/month that gave them breathing room, dignity, and peace.

💬 Explore our full range of life insurance options in Idaho →

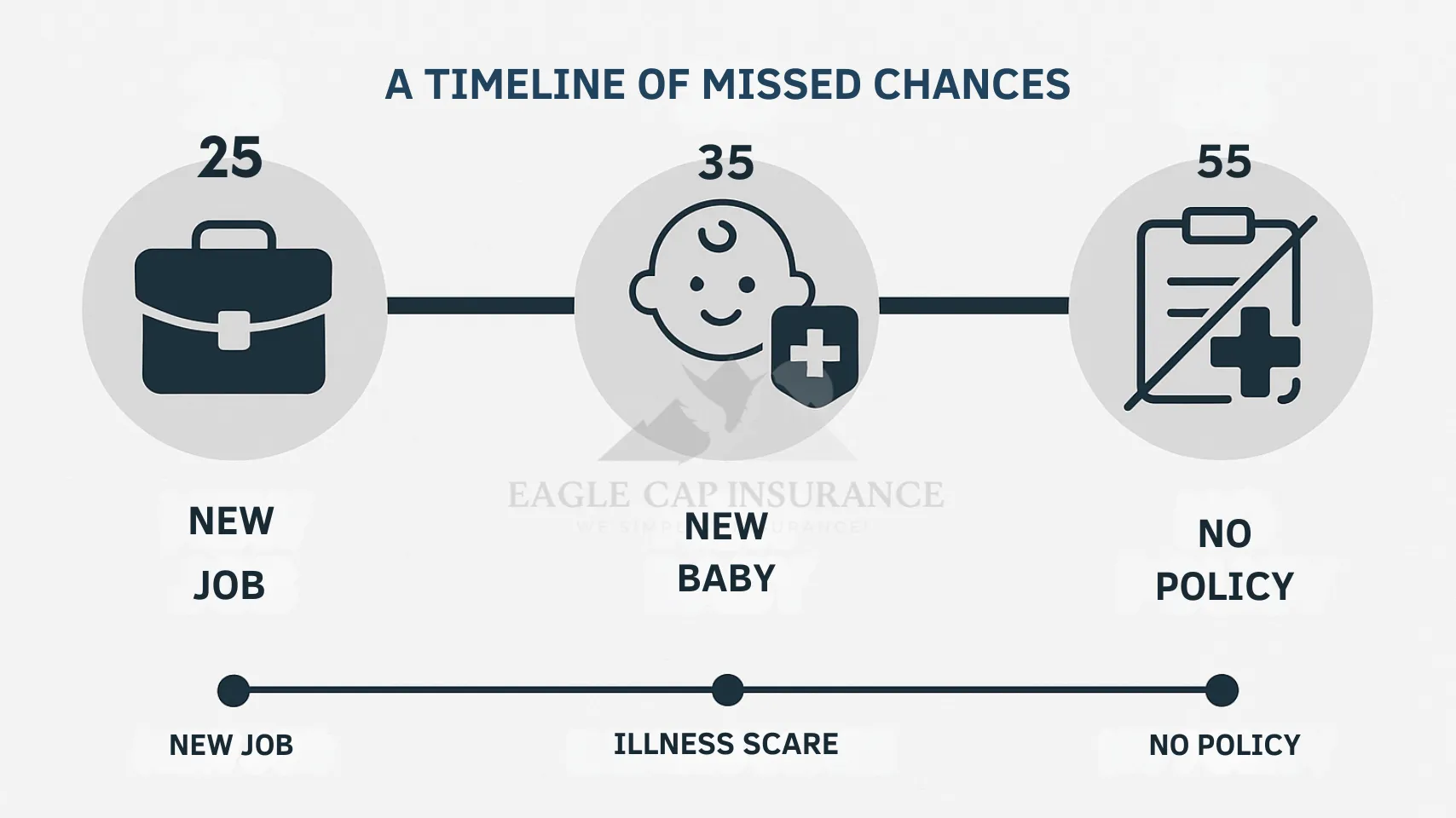

A Timeline of Missed Chances

Age 25: New job → Didn’t opt into group life insurance

Age 35: New baby → Thought they’d “get to it later”

Age 45: Health scare → Premiums spike

Age 55: Still uninsured → Fewer policy options available

👇 This is a pattern we see often. Don’t let it be yours.

Common Triggers for Getting Life Insurance in Idaho

You don’t have to wait until you’re married or have a mortgage. These are common moments where Idaho clients take action:

- Just had a child (Idaho Falls couple in their 30s)

- Bought a home in Preston

- Started a new job or business

- Had a health scare in the family

- Nearing retirement and planning estate transfer

What We Recommend for Idaho Families

Kyle also advises on optional policy riders like Accidental Death Benefit (ADB), Return of Premium (ROP), and Child Term Riders based on your needs.

The Intersection of Life, Disability, and Health Coverage

Many Idaho clients ask:

“If I already have health insurance, do I really need life insurance too?”

Here’s the breakdown:

- Health insurance Idaho Falls & Preston pays medical bills while you’re alive.

- Disability insurance Idaho Falls & Preston protects income if you can’t work.

- Life insurance Idaho Falls & Preston protects your family if you pass away.

These aren’t redundant, they’re layered protections for life’s what-ifs.

💬 Read more about disability coverage in Idaho →

Business Owners: You’re Exposed Too

If you’re self-employed or run a business in Idaho Falls or Preston, life insurance decisions have a ripple effect beyond your family.

Kyle works with business owners to structure:

- No funded buy-sell? Your partner could inherit your shares without a way to buy them out.

- No key person coverage? Your business may lose its momentum — or worse, its clients — overnight.

- No executive bonus plan? You risk losing top talent to companies that offer better protection.

✅ Eagle Cap Insurance structures real plans for Idaho businesses, including:

- IRS-compliant Buy-Sell Agreements (cross-purchase and entity purchase)

- Key Person Policies that cover both death and disability

- Executive Bonus Plans using life insurance as a retention tool

Most local business owners didn’t know they could fully deduct premiums through bonus structures or pass ownership to heirs via life insurance.

📌 Learn how business life insurance works →

Real Example From the Field

Kyle worked with a 52-year-old client from Preston. His friend had passed without coverage. He didn’t want to leave his kids guessing.Covered his mortgage and two kids’ college fund

- Locked in rates before his upcoming surgery

- Cost him under $80/month

He now tells his coworkers: “This isn’t about dying. It’s about not leaving a mess.”

When You Wait, You Risk These Three Things:

- Higher Premiums Each year you delay, your rate increases. Health changes can push you into uninsurable territory.

- Limited Options Some plans require medical exams, and pre-existing conditions can lock you out of better policies.

- Emotional Burden on Family Instead of making space to grieve, they’re forced to figure out funeral costs, debt, and next steps.

Kyle’s Process: No Pressure. Just Planning That Works.

We know this can feel overwhelming. That’s why Kyle’s approach is rooted in education first.

Here’s what working with us looks like:

✅ Identify your financial risk zones

✅ Match policy types to your needs (term, whole, or hybrid)

✅ Explain underwriting in plain language

✅ Coordinate with your health & disability plans

✅ Review every few years to keep your plan current

💬 “Kyle helped us review all options and never pushed us into something we weren’t ready for. We walked away feeling informed and protected.” — Kate Jones, Idaho Falls client

💬 “He helped us combine life and disability insurance into one solid plan. We sleep better at night.” — Sam Leesch, Preston client

FAQs Idaho Families Ask About Life Insurance

When’s the best time to buy life insurance?

The earlier the better. Your age and health status directly affect your premium.

Is life insurance taxable in Idaho?

Generally no. Idaho does not have an inheritance tax, and most death benefits are tax-free for your beneficiaries.

How much coverage do I need?

A good rule of thumb is 7–10x your annual income, but we tailor it to your mortgage, dependents, and financial goals.

Ready to Get Ahead of This?

Most of our Idaho clients say the same thing once we’ve finished:

“I wish I had done this sooner.”

If you’re in Idaho Falls, Preston, or anywhere nearby, this is the moment to make sure your people are protected.

📅 Book a 1:1 call to:

- Review existing coverage gaps

- Learn the differences between term, whole, and universal life

- Explore life insurance options Idaho families actually use

- Bundle with your health, disability, or business insurance for better rates

📍 Serving clients across Preston, Idaho Falls, and surrounding areas.

About the Author

Kyle Bennett is a licensed insurance advisor and founder of Eagle Cap Insurance, based in Idaho Falls and Preston, Idaho. He has over 20 years of experience helping Idaho families and small business owners find the right mix of life, disability, health, and business insurance.

- Licensed Health & Life Insurance Agent (Idaho)

- Trusted by hundreds of Idaho families

- Local expert in ACA, ICHRA, key person insurance & more